Is gold worth buying today? How do I maximize my returns on gold investments?

Let’s dig a little deeper to find out:

Investment in this universal currency is a safe haven as it protects your investments against inflation, currency fluctuation, uncertain market conditions, etc. A 10% holding in gold provides adequate portfolio diversification as gold tends to behave differently than stock movement. The various investment options in gold majorly include physical gold, exchange-traded funds (ETFs), gold mutual fund & sovereign gold bonds. Each one has its own merits and demerits hence an informed decision is essential. Let’s understand each one of them:

1) Physical Gold:

- Jewellery, coins or biscuits are generally bought on occasions and have religious or emotional value.

- Confidentiality can be maintained as it is usually bought through a jeweller or banker.

- It is important to maintain proof of purchase (e.g. invoice) for taxation or resale purpose.

2) Exchange-Traded Funds (ETFs):

- It’s a combination of investment in physical gold & stock.

- A Demat account is mandatory.

- Physical Gold Bullion of an equivalent amount of investment made is kept with the custodian (e.g. bank) in the name of the investor.

- The custodian is responsible for the protection of bullion hence the risk of theft is mitigated.

3) Gold Mutual Funds:

- It is a variant of exchange-traded fund, whereby the underlying asset is exchange-traded fund instead of physical bullion.

- Like exchange-traded funds, these are pooled investments managed by mutual fund AMC.

- The portfolio of these mutual funds mainly consists of exchange-traded funds & other related assets.

4) Sovereign Gold Bonds (SGBs):

- Intending to curb physical gold transactions, RBI has released sovereign gold bonds.

- They are issued at various intervals as per RBI’s schedule.

With so many options available confused which one should you invest in?

Let’s score them on relevant factors:

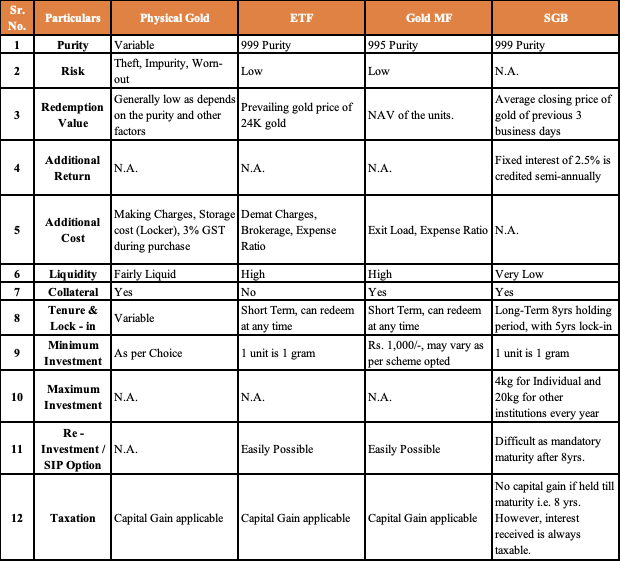

1) Purity: Looking for 99.9 % purity or 24k Gold then sovereign gold bonds, exchange-traded funds or gold bar is your best bet, whereas gold mutual fund will provide 95.9% purity, choose the desired purity that suits your pocket while investing in physical gold.

2) Risk: Beware of the impurity risk, theft, being worn out, etc. while investing in physical gold. Choose your intermediary wisely while dealing in digital gold.

3) Redemption Value: Physical gold is sold at the prevailing gold price, whereas gold exchange-traded funds are redeemed at 99.5% pure gold bar’s value, in the case of gold mutual fund redemption value is their NAV price and sovereign gold bonds are redeemed at the average closing price of gold of previous 3 business days.

4) Additional Return: Fixed interest of 2.5% is credited semi-annually under sovereign gold bonds makes them irresistible.

5) Additional Cost: Management Cost of generally 0.5% to 1% applies to gold mutual fund and exchange-traded funds. Moreover, gold mutual funds may also cost an exit load of 1% – 2%. Demat charges and brokerage to be born to hold exchange-traded funds. Physical gold will bear making charges, GST @ 3% and locker charges may also be applicable.

6) Liquidity: Physical gold is fairly liquid, also gold mutual funds can be sold anytime, whereas exchange-traded funds can be traded on stock exchanges and hence liquidity of each exchange-traded funds differs based on their performance, sovereign gold bonds is relatively less liquid and can be traded on the stock exchange only if held in Demat form.

7) Collateral: All the above investments can be pledged to acquire loans except Gold exchange-traded funds.

8) Lock-in & Tenure: Sovereign gold bonds have a lock-in of 8 yrs however early redemption from the 5th year is possible, whereas the investor has the liberty to choose any tenure in all other investment options.

9) Minimum investment: One can purchase as low as 1 gram gold through exchange-traded funds or sovereign gold bonds, however, one can invest in a gold mutual fund with Rs. 1000/- depending on the scheme opted, physical gold can be bought for any value desired.

10) Maximum Investment: An individual can invest a maximum of 4kg gold per year in sovereign gold bonds whereas the limit of 20kg is set for other institutions. There is no such limit in any other gold investment options mentioned.

11) Re-investment & SIP option: One can re-invest in exchange-traded funds or invest in gold mutual funds through SIP to average the cost incurred. However, sovereign gold bonds can be bought primarily through RBI only as per scheduled dates released by RBI, also purchasing sovereign gold bonds through the secondary market may not be always feasible for re-investment. This benefit is not available in physical gold.

12) Taxation: Capital Gain Tax is applicable on each of the above investment options, however, no tax is payable if sovereign gold bonds are held till maturity i.e. 8 yrs. The interest of 2.5 % received on sovereign gold bonds is taxable.

In a Nutshell :

The bottom line,

If the investing goal is long-term, one should lean towards sovereign gold bonds, and the ones intending for short-term investments or accumulating gold at different intervals may opt for exchange-traded funds or mutual funds.

For the Financial Year 2021-22 RBI has lined up six series of sovereign gold bonds from May 2021 to September 2021, here are the Subscription dates of the first set of sovereign gold bonds launched this year:

- Series I: May 17 – May 21, 2021

- Series II: May 24 – May 28, 2021

- Series III: May 31 – June 04, 2021

- Series IV: June 12 – June 16, 2021

- Series V: August 09 – August 13, 2021

- Series VI: August 30 – September 03, 2021